New report: How consumer organisations can maximise their impact in digital finance policy-making

As financial technology rapidly evolves, and regulators race to keep up, an ever more complex web of policy instruments and actors within the digital finance policy space is formed. Within this web there are gaps, overlaps, and hidden threats, leaving consumers - all of us - at risk of harm. The lack of an established legal and regulatory framework presents challenges, while also offering an opportunity for consumer organisations to deeply integrate themselves within the policy-making process.

Consumer organisations can be a linchpin within an inclusive and protected financial services ecosystem. They provide essential support to people in the marketplace, from advice on how to seek redress to education on consumer rights within digital financial services. They are often trusted pillars within their communities and are uniquely placed to collect consumer data essential to evidence-based policy-making.

But with thinly stretched resources and unstable funding, many find it difficult to engage regulators and policy-makers. When we speak to our Members - consumer organisations based in over 100 countries around the world - they repeatedly tell us that they feel held back from improving financial consumer protection.

Today, we launch a new report - Maximising consumer voices in digital financial services policy-making: Consumer organisations' engagement strategies - built upon interviews with Consumers International Members across 13 countries.

As the digital finance policy space becomes more complex, this report showcases powerful examples of innovative consumer organisations who are making strategic use of existing resources, connections, and expertise to drive change towards better digital financial services for consumers.

These guidelines have been specifically designed to support consumer associations in low- and middle-income countries. But with the digital financial services space continually evolving, they will also provide useful reading for those in high-income countries struggling to gain a foothold.

The report forms part of our work through the Fair Digital Finance Accelerator to support and empower consumer organisations in low- and middle-income countries to engage with regulators and champion a safe, fair and sustainable digital finance marketplace.

The Challenge

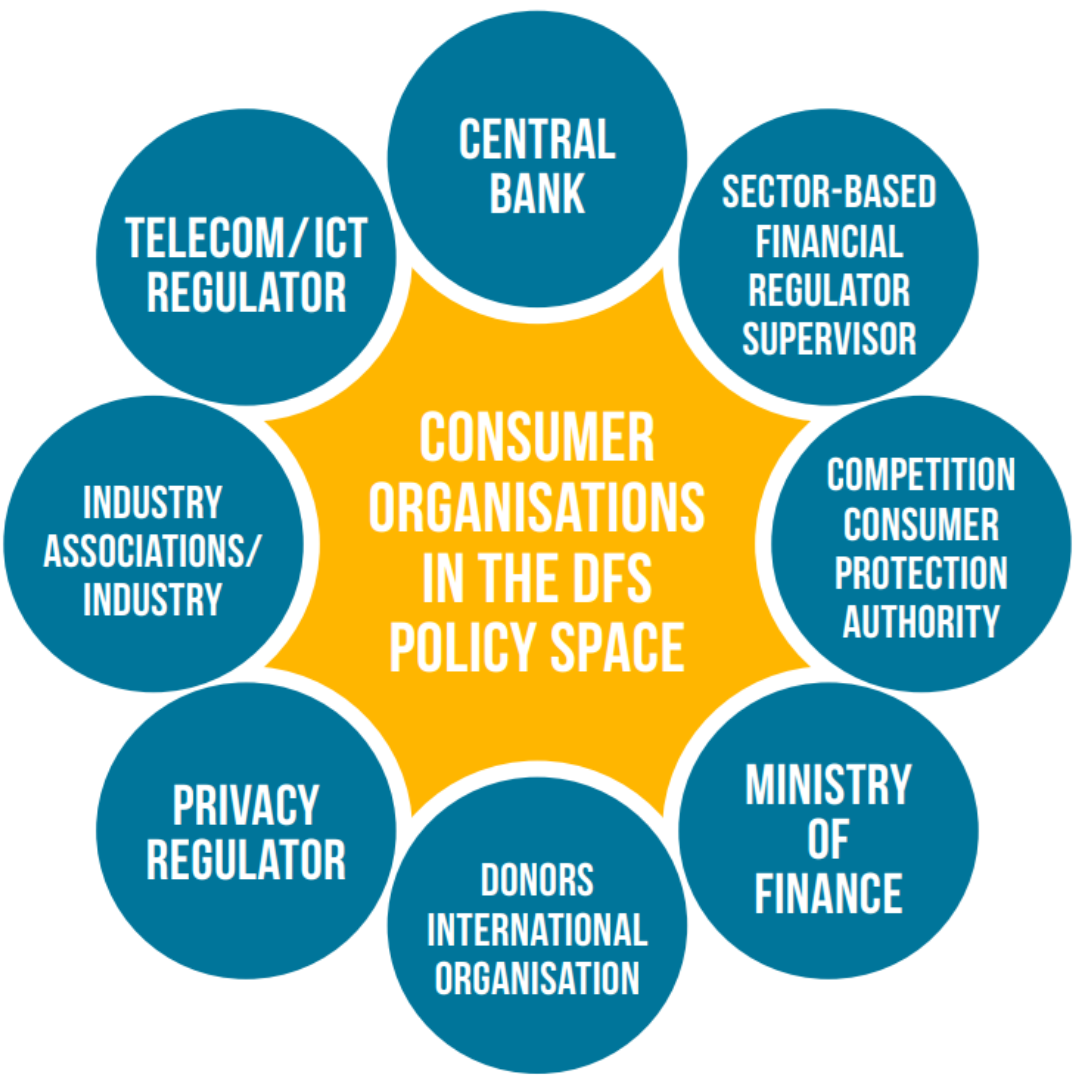

Influencing public policy is rarely a linear process, evolving through complex interactions and negotiations among a range of stakeholders. For those with limited power and resources, intercepting and exerting influence over this process can be difficult, especially where it is dominated by powerful groups.

These issues are exacerbated within digital financial services. The cross-cutting nature of the sector means it involves many different actors, and in low- and middle-income countries in particular, the regulatory environment is often underdeveloped and overly complex.

Guidelines for maximising the consumer voice in digital finance policy-making

The report outlines five key areas where consumer organisations can focus their efforts.

1. Build on existing foundations

To influence the digital financial services space, consumer organisations should look at how they can build on their existing networks, expertise and skills.

For example:

In Rwanda, ADECOR has more than 30 consumer ambassadors or consumer representatives in each district helping with field research, data collection, awareness campaigns, consumer complaint management and other related activities. They have deployed these resources to research digital finance risks, such as monitoring the levels of fraud consumers have experienced in digital financial services in seven districts across the country.

2. Foster institutional structures and processes

Consumer organisations should support the creation of stable institutional foundations for digital financial services policy-making structures and processes. Because such institutions are still fluid in the digital financial services space, this is where consumer organisations can build an impact, positioning themselves as dependable, valued and essential partners within these structures.

For example:

The Ivorian Consumers Association (Côte d’Ivoire) is a permanent consultative member of the Observatory for the Quality of Financial Services, which ensures the functioning of the digital finance system in Côte d’Ivoire. The Ivorian Consumers Association serves as a bridge between consumers and this permanent government body.

Elsewhere, Consumers Lebanon demonstrates an inspiring example of how consumer organisations can supplement the capacity of state institutions in times of crisis. Lebanon is currently experiencing a deep economic crisis and political unrest has weakened regulatory authorities, the judiciary and state institutions. Not only has this disrupted the proper application of consumer protection law, it has corroded consumer trust in state institutions. Consumers Lebanon has stepped in to fill this gap, providing guidance and awareness raising to consumers.

3. Provide an essential source of original consumer data

Due to the newness of the field, many consumer challenges regarding digital financial services have not yet been clearly documented. Consumer associations can fill this gap. Tools like a well-functioning consumer complaint management system can be a unique data source. Low-cost options include ‘consumer listening’ through social media monitoring.

For example:

Between 2006 and 2010, Korea saw a widespread mis-selling scandal in which credit card companies sold add-on products to millions of consumers via mobile and telemarketing. Consumers Korea investigated internet blogs and portals (such as Naver) to identify flaws in Korea's financial consumer redress system, proposing ways of improving the system to policy-makers.

4. Leverage relationships

In the short term, building a team of experts working exclusively on digital finance will be difficult for many organisations. Consumer associations should supplement their existing expertise by focussing on strategic partnerships with civil society, academic institutions, industry and other stakeholders.

For example:

Consumer organisations can collaborate across borders to flag new risks in digital finance. In 2022, Consumers International led a group of consumer organisations from 11 countries to call on governments to protect consumers against the growing risks of Buy Now Play Later. Following this action, many regulators, including the US Federal Reserve, the CFPB, and the Australian government initiated actions to research and regulate Buy Now Pay Later in 2022 and 2023. This joint call for action shows that information sharing between consumer organisations’ networks can identify digital finance consumer risks before they become widespread in other regions.

5. Focus on initiatives for vulnerable consumers

Digital financial services have the potential to offer real benefits for vulnerable consumers, but financial inclusion will be tempered if advances are not accompanied by strong consumer protection. Consumer organisations are often already serving underprivileged populations in their regions – and are trusted advisors on issues like cost-of-living, energy, food, and product safety.

For example:

Low levels of financial inclusion and literacy present a significant barrier holding back poor and vulnerable communities from escaping poverty. This is particularly the case for the rural women in India that CUTS (India) work with. The organisation is working in partnership with the Indian government to improve the financial literacy of women in rural areas by linking them with financial services and support and development schemes.

Get involved

The Fair Digital Finance Accelerator is working to improve the state of digital finance in low- and middle-income countries. We train and build capacity among 65 consumer organisations worldwide, linking consumer advocates to national and international policy-makers. To join the Accelerator, or find out how you can support this work, contact impact@consint.org.